The 1031 exchange allows an investor to defer the capital gains taxes that would otherwise be due on the sale of investment property.

In a traditional sale, taxes may exceed 20--30% of capital gains (use our capital gains tax calculator to estimate yours). However, if the proceeds from the sale are reinvested according to the rules laid out in IRC § 1031, those taxes can be avoided.

This article answers the following questions:

- What Are the Rules for a 1031 Exchange?

- What Are the Stages of a 1031 Exchange?

- What Are the Deadlines in a 1031 Exchange?

- What Are the 1031 Exchange Property Identification Rules?

- How Can an Investor Completely Eliminate Capital Gains Taxes?

To defer the recognition of capital gain, an investor must follow three basic 1031 exchange rules.

What Are the Rules for a 1031 Exchange?

-

Property Must Be Like-Kind

The replacement property must be like-kind to the relinquished property. Generally, real estate held for business or investment purposes in the United States is considered "like-kind,” including commercial and residential property.

While residential property held for business or investment purposes qualifies for a like-kind exchange, one’s own residence or vacation home does not. (However, there are other tax shelters available for the sale of a personal residence or vacation home.) -

Equity and Debt* Must Be Reinvested

Second, the total value of the replacement property must be equal to or greater than the total value of the relinquished property to fully avoid capital gains taxes. Any capital that is not reinvested is taxable “boot.”

*The total debt amount does not always have to be reinvested, so long as the total equity is reinvested and the total investment amount is equal to or greater than the total value of the relinquished property. Investors are permitted to take on less debt if they put in more capital. -

Titles Must Be Held by the Same Owner

Lastly, the ownership title for the replacement property must be identical to the title for the relinquished property. Investors are permitted to hold title to their replacement property by way of pass-through entities, such as single-member LLCs and even DSTs with multiple investors, as these are disregarded in such cases.

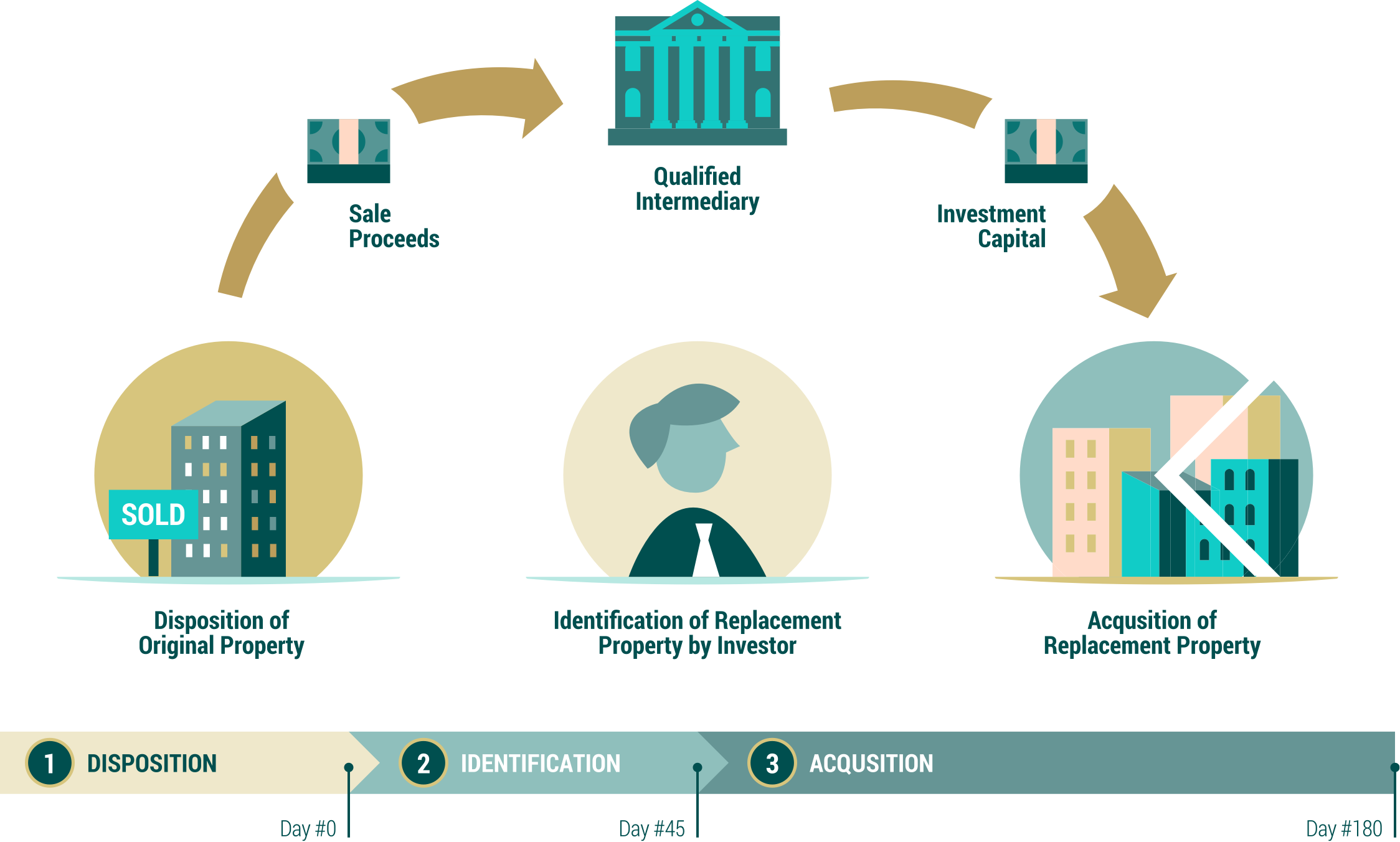

What Are the Stages of a 1031 Exchange?

-

Before Starting: Plan Your Exchange

Make plans to carry out a 1031 exchange, and engage a Qualified Intermediary (QI) in advance of the disposition of the property to be replaced.

-

Day #0: Complete the Disposition of the Original Property

Sell the investment property to be replaced and have the proceeds held by the QI to avoid taking constructive receipt.

-

Day #45: Complete the Identification of Potential Replacement Property

Work with a broker to identify potential replacement properties within 45 days after the sale of the relinquished property.

-

Day #180: Complete the Acquisition of the Replacement Property

Close escrow on the replacement property within 180 total days after disposition of the relinquished property.

What Are the Deadlines in a 1031 Exchange?

There are strict time limits for the identification and acquisition of the replacement property. The potential replacement property must be identified by midnight on day #45 after the close of escrow on the relinquished property, and the replacement property must be acquired by midnight of day #180. The day after the close of escrow on the relinquished property is day #1. The exchange period includes weekends and holidays, and there are no exceptions.

You can calculate your 45th and 180th day deadlines

using our 1031 Exchange Date calculator.

What Are the 1031 Exchange Property Identification Rules?

You have your choice between three different rules for identifying and acquiring 1031 replacement properties. You only need to comply with one of these rules. You may identify up to three replacement properties and purchase any, or all, of them, regardless of their total value, to complete your exchange (the “3-Property Rule”).

Or, if you’d rather, you may identify more than three replacement properties, if their total value does not exceed 200% of the total value of the relinquished property. You may purchase as many of the identified properties as you want (the “200% Rule”).

Finally, if neither of the other two rules suit your needs, you may identify any number of replacement properties, regardless of their total value, as long as you acquire 95% of the total value of all of the properties identified (the “95% Rule”).

How Can an Investor Completely Eliminate Capital Gains Taxes?

You can continue to defer the recognition of your capital gains using the 1031 exchange until you are ready to pass your investment property on to your heirs. When your beneficiaries inherit your property, its tax basis steps up to the current market value.